For Childcare Centre developers, operators, investors, financiers, and advisors

Share

🏗️ Mount Peter PDA (Cairns): Fast-track growth, first-mover upside

Published 2 months ago • 18 min read

📆 Fri, 15 Aug 2025 | BNE | Fine 12° ☀️ Good morning... Why one simple trick could accelerate how you run, and grow, your childcare business.

The gist: A new Big Think piece spotlights a counterintuitive but powerfully effective learning hack: imitate someone better than you. Rather than breaking down skills into parts, the essay argues we often improve fastest by modelling how a more skilled, or simply more confident, person would act.

Why it matters to CREW: Whether you’re pitching to investors, designing your next centre, refining your curriculum, or building your leadership team, adopting a “what-would-a-great-developer/operator/investor do?” mindset can unlock immediate performance gains. It’s a fast, low-cost skill upgrade that scales across roles; from operations to finance to strategic planning.

🎉 Big congratulations: to CREW reader Justin Bailey on his appointment as CEO-Designate at Arena REIT, a well-deserved recognition and a big move in Australia’s childcare property landscape. 🧭 In today's CREW

🏗️ QLD: Mount Peter PDA (Cairns) 💰 Big Sydney Childcare Sale 🚧 10 Pitfalls In Childcare Development 🏢 Arena REIT FY2025 🚀 QLD: Southern Thornlands PDA 📍Perth’s Next Big Leap 🏗️ DA Watch: Middle Ridge, Toowoomba 🏡 QLD: Big Push in Canungra 🆕 New DAs and Service Approvals 💬 Parting Thought

🏗️ Mount Peter PDA (Cairns): Fast-track growth, first-mover upside

Declared: 30 Jul 2025; ILUP now in force for ~18 months while EDQ drafts the Development Scheme. Scale: ~2,650 ha between Edmonton → Mackey Creek, bounded by the Bruce Hwy (east) and Wet Tropics WHA (west). Key roads: Mount Peter Rd, Draper Rd, Petersen Rd, Harris Rd, Hall Rd, Jones Rd, Davies Rd. Capacity: ~18,500 homes / ~42k residents. Early release: ~200 homes fast-tracked under the ILUP.

🎯 Why it matters

That housing pipeline = multiple long-day-care centres over the build-out, best positioned near neighbourhood centres, schools and collector roads flagged in the ILUP vision.

Servicing is the gatekeeper: limited water/wastewater capacity noted; approvals may need interim wastewater solutions and infrastructure agreements/offsets. Timing & staging will drive feasibility.

🗺️ Precincts & timing

Precinct 1 – Residential North: DA pathway open now under the ILUP; focus for early housing.

Precinct 2 – Investigation area: more planning/environmental work before urban development proceeds.

👥 Who you’ll deal with

EDQ (assessor & lead): ILUP now; Development Scheme to follow; DCOP will set charges/offsets.

Cairns Regional Council: partner on trunk networks; corridor is a priority in its program.

Cairns South SDA (adjacent jobs hub): Wrights Creek/Gordonvale industrial precincts should lift local ECEC demand as employment lands roll out.

🏢 Land & players (on the ground)

Roman Catholic Diocese of Cairns – MacKillop Catholic College (Mount Peter): major education anchor → obvious ECEC co-location target. Offering Prep to Year 10, 2023 enrolments - 889.

Kenfrost Homes – Mount Peter Residential Estate: active estate developer with an info centre on Greypeaks Dr—useful for embedded ECEC in new stages (confirm PDA/Precinct alignment at pre-lodgement).

Council and EDQ are coordinating enabling infrastructure; align ECEC timing with trunk delivery windows.

✅ Bottom line

Mount Peter is Cairns’ last big greenfield. Teams that secure sites in Precinct 1, pair with a quality operator, and solve servicing with EDQ will set the ECEC network footprint and capture the best corners.

💰 Sydney Childcare Sale Smashes Records and Signals Stronger Market Momentum

Why it matters: A $16 million childcare transaction didn’t just mark a milestone; it reinforced the resilience and appeal of early learning assets in Australia's evolving commercial property landscape.

Here’s why this matters for developers, investors, and operators alike.

📌 The Big Deal

Price tag: A Sydney childcare centre sold for $16 million, setting a new national benchmark for freehold early learning assets.

Takeaway: This isn’t just about one high-profile deal. It underscores how HNWIs are chasing long-dated, income-secure essential-service assets.

📈 Market Momentum

2025 is proving robust: Stonebridge and others have transacted over $205 million in childcare properties so far, up 58% on Q1 2024.

Diverse buyers: From private buyers and syndicates to offshore capital, the buyer pool is widening, drawn by strong tenant covenants and strategic locations.

Yield compression: Sub-5% yields are increasingly common for prime metro assets with strong underlying land values and quality covenants, reflecting intense competition amongst HNWI buyers.

📉 Interest Rate Tailwinds

Cheaper debt: The RBA’s official cash rate, the benchmark interest rate that flows through to business loans, mortgages, and commercial finance, now sits at 3.6% after the August cut. It’s the lowest since March 2023, and it’s reducing borrowing costs for investors and developers. For long-leased, yield-sensitive assets like childcare centres, lower funding costs support sharper pricing, stronger valuations, and more competitive bidding.

Pricing support: Lower rates put downward pressure on yields and upward pressure on values, especially in defensive sectors like childcare.

Liquidity lift: Transaction volumes are up across commercial property, with essential-service assets leading the charge.

🚀 Why This Sale Matters

Benchmark reset: $16M sets a new price watermark — and redefines what qualifies as a “trophy” childcare asset.

Policy and scarcity: Federal childcare funding and slower new-build pipelines boost the appeal of existing well-located centres.

Capital competition: More buyers + cheaper debt = faster deals and sharper pricing for quality stock.

The CREW take:

Interest-rate cuts are pouring fuel on an already-competitive market for premium childcare assets. The fundamentals still rule; location, lease term, operator strength, but the capital chasing them is only getting hungrier.

🚧 10 Pitfalls to Dodge in Childcare Development

Why it matters: Childcare development isn’t just buying sites and pouring concrete. It’s navigating a high-stakes mix of regulation, market dynamics, and operational realities.

It looks deceptively simple.

But there are pitfalls.

Yet, it’s not that complex a property type if you get the fundamentals right.

Here are 10 pitfalls to watch out for...

1️⃣ Skipping the market check

Mistake: Choosing a site without hard data on demand, competitive framework, future supply pipeline, and catchment strength. Better play: Start with a formal needs assessment: map 0–4 population and growth, fees/incomes, existing capacity, DA/approval pipeline, school catchments, and access. In a maturing, more competitive market, oversupply kills returns. Skipping this step has already driven nine-figure capital misallocation.

2️⃣ Rushing the buy button

Mistake: Acquiring land before deep-dive feasibility; missing planning overlays, service constraints, or community objections. Better play: Test sites against zoning, accessibility, SEIFA, and realistic capacity. A bad site never becomes a good deal. Give yourself enough time and budget to do professional-level due diligence upfront before UC commitment.

3️⃣ Designing in a vacuum

Mistake: Over-designing (especially structure) or dropping a cookie-cutter plan that ignores flow, compliance, or build cost. Better play: Use childcare-specific design that blends planning and licensing requirements, community expectations (esp. adjoining neighbours) operational efficiency, and construction cost discipline.

4️⃣ Chasing maximum places

Mistake: Designing for headcount, not market alignment. Better play: Size capacity to what the catchment can absorb at sustainable occupancy and fee levels, allowing some upside for growth via staged additions.

5️⃣ Underestimating planning complexity

Mistake: Thinking council approval is a formality. Better play: Factor in pre-lodgement consultation, potential appeals, and the local political climate. Timeframes can double overnight.

6️⃣ Waiting to find a tenant

Mistake: DA first, tenant later. This risks slow lease-up and weak terms. Better play: Engage credible and quality operators early. Biggest is not necessarily best. Pre-commitments de-risk funding and improve valuation. Avoids redesign later.

7️⃣ Ignoring fit-out from day one

Mistake: Treating internal fit-out, outdoor playscapes, and compliance specs as an afterthought, or leaving them as PC items to be fully detailed and priced later. This will bite hard. Better play: Lock these in pre-build; they influence lease terms, delivery timelines, capex, and feasibility.

8️⃣ Forgetting who it’s for

Mistake: Prioritising ROI over a child-centred environment. Better play: Design for safety, natural light, and flexible learning spaces. Ensure the centre has not just the function, but the comfort, and amenity needed to attract and retain quality educators. Parent word-of-mouth is your best marketing spend.

9️⃣ DIY project management

Mistake: Trying to run the process solo, from DA to handover. Better play: A specialist PM saves months, mitigates risk, and keeps consultants, builder, and operator aligned.

🔟 Overlooking brand and lease optics

Mistake: Weak branding and loose lease structures when approaching financiers or buyers. Better play: Present like an institutional-grade asset. It drives investor confidence and operator success.

The CREW take:

📊 We’ve seen well-located, fully approved projects stall because they missed on tenant timing. We’ve seen brilliant operators struggle with over-sized centres in soft catchments. In today’s climate of scarce and expensive sites, high build costs, and tighter funding, the winners will be those who get the fundamentals right with relentless professional execution to deliver a quality product everyone loves.

📌 Optivest can help you get them right

We identify high-potential childcare market gaps, vet sites with institutional-grade analysis, and connect you with quality operators and capital partners. Whether you’re looking to acquire, develop, or expand, we help you avoid costly mistakes and move faster to approvals, tenants, and returns. 📩 hello@optivest.com.au | 🌐 optivest.com.au

🏢 Arena REIT FY2025: Growth, record pipeline, and a leadership change

Why it matters: Arena REIT delivered another year of earnings growth, long-WALE stability, and its largest development pipeline in five years — while announcing a CEO succession.

📈 FY2025 highlights

EPS: 18.55c, +5.1%

NAV: $3.46, +1.5%

DPS: 18.25c, +4.9% (FY2026 guide: 19.25c, +5.5%)

Gearing: 22.8%

Portfolio: $1.9B assets, WALE 18.4 years, 100% occupancy

Development pipeline: 29 projects, forecast $227M cost, all 20-year initial leases

👤 Leadership change

Arena REIT has announced the resignation of Rob de Vos as Managing Director and CEO. Justin Bailey, current Chief Investment Officer, has been appointed CEO-designate.

🔍 CEO Watch

Bailey joined Arena in 2024 as CIO and, in FY2025, oversaw 11 acquisitions, 12 early learning centre completions, and the replenishment of a 29-project pipeline — all within Arena’s disciplined yield and lease framework. His track record is grounded in transaction execution and portfolio strategy, aligning with the company’s long-WALE, purpose-built focus.

47% reduction in financed emissions since FY2021 baseline

🛠 Market & policy context

Federal reforms to boost affordability, access, and quality — including removal of the activity test (Jan 2026) and $1B build fund for low-supply areas

State reviews focusing on safety, workforce checks, and stronger regulation

ELC net rent-to-gross revenue ratio: 9.9%

Average daily fee per place: $155.29, +9.75% YoY

💡 Beyond the Numbers

Strategy continuity under new CEO; exploring other social infrastructure with similar lease and property traits.

20-year standard lease is mandatory; active WALE extensions via strategic capex ongoing across portfolio.

Under-rented portfolio: Average rent $3,240/place vs new rents $4,000+/place; operators able to absorb increases.

Capital discipline: Net seller in past six months into HNWI-driven, record-price market; recycling into high-quality pipeline.

Market rent growth outlook: 25 of 32 reviews capped; highest uplift 20%; long-term growth runway supported by operator economics.

Development staging: $175M capex over 4 years; fund-through pricing 6%+ must work for REIT, developer, and operator. Big chunk of pipeline involves one quality operator, but sufficient spread to avoid concentration risk.

Tenant conditions: Workforce competition easing; regulatory changes expected to lift quality bar. Good operators are ready and resilient with positive outlook.

📜 CREW POV

Arena’s long-WALE discipline, low rent-to-revenue ratios, and capital recycling strategy position it for sustained rental growth.

FY2025 shows consistent growth, a fortified portfolio, and a leadership handover designed to keep the machine running, with upside in rents and potential social infrastructure sector property type diversification ahead.

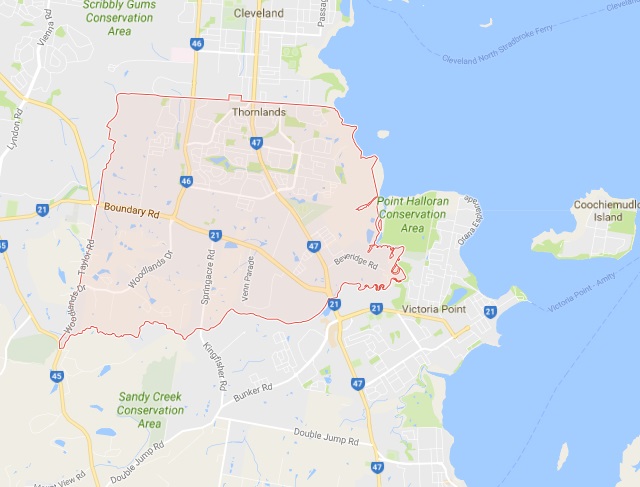

🚀 QLD: Southern Thornlands: Redland’s Next Growth Frontier

With room for 8,000 new homes, a mixed-use early release precinct, and major state-led infrastructure upgrades, the Southern Thornlands PDA is set to reshape Redland City in South East Queensland (SEQ).

Southern Thornlands PDA, Redland City, SEQ

Southern Thornlands PDA, Redland City, SEQ

Early movers who align with EDQ’s vision for integrated, walkable neighbourhoods stand to secure the best commercial and community sites before the full development scheme locks in.

What EDQ is doing

Purpose & scale. The Southern Thornlands PDA (≈890 ha) was declared 4 Apr 2025 to accelerate housing and jobs in Redland City, targeting ~8,000 new dwellings and new employment areas. An Interim Land Use Plan (ILUP) now guides early lodgements while the full PDA Development Scheme and infrastructure plan (incl. DCOP) are prepared.

Timeline. The ILUP is intended to operate for up to ~18 months while EDQ co-designs the Scheme and DCOP with stakeholders; public consultation is via EDQ’s “Have Your Say.” (ILUP commencement noted 4 Oct 2025, with an expiry noted 4 Oct 2026, per the ILUP PDF.)

Where & what first. EDQ has identified an Early Release Area east of Springacre Rd (Precinct 1) so development can start while the broader scheme is completed—first ~900 homes, with an initial $4m Springacre/Boundary Rd intersection upgrade flagged. This intersection upgrade is key to unlocking 900 new homes in Stage 1 of the PDA, easing local traffic congestion for commuters, school runs, and businesses.

Springacre/Boundary Rd intersection upgrade

Boundary & context. The Thornlands Priority Development Area is generally bounded by:

What’s in the ILUP (matters that affect childcare)

Two precincts.

Precinct 1: Eastern (Early Release). Residential neighbourhood with a mixed-use neighbourhood centre; net density target 25–35 d/ha, village-heart height up to 6 storeys, and retail/commercial GFA capped ~2,500 m². ILUP Map 2 also shows a primary access location to Springacre Rd.

Precinct 2: Western (wider PDA). Intended to accommodate employment land, centres, schools and community facilities, with detailed locations to be set by the forthcoming Scheme and infrastructure plan.

Housing mix & affordability. ILUP targets ~20% affordable/market-affordable, including ~5% social housing across development—an important policy lever for “key worker” childcare staff narratives.

Environment. Strong protection/rehabilitation of the Eprapah Creek regional ecological corridor with setbacks and habitat investigations—site selection must avoid the corridor and “habitat value investigation areas.”

Movement & servicing. Development must fund/uphold Springacre Rd upgrades and full urban services; final contributions/offsets will be set via the DCOP in the Scheme.

Landowners & early movers

Precinct 1 application (lodged). Mirabel Thornlands Pty Ltd (via RPS) has a Preliminary Approval application covering ~40.82 ha at 62-138 Springacre Rd (multiple titles). Landowners include several private owners and URBEX 119 Pty Ltd (BMD Group). Their plan positions a neighbourhood centre with a childcare centre plus medium-density housing.

Major PDA landholders. Urbex (BMD) and Harridan (Holmwood Highgate Group) publicly welcomed the PDA. Both are significant Thornlands players and likely master-developers/partners across later stages.

Schools: What we know (and don’t)

Thresholds & quantum. Mirabel’s Economic Technical Note estimates ~3 government primary schools and 1 secondary school at PDA build-out; Precinct 1 alone (~2,900 people) isn’t enough for a state primary (rule-of-thumb ~7,500 people catchment). Locations will be fixed through the PDA Scheme with the Department of Education.

Local government position (infrastructure watch-outs)

Cost-shifting risks. Redland City has stated infrastructure must not burden existing ratepayers and is pushing for state-backed “region-shaping” items (Eastern Busway to Capalaba; Cleveland line duplication; key state road upgrades). Expect hard conversations on sequencing and developer contributions. Usual argy-bargy to follow.

What this means for childcare developers/operators/investors

Where demand will form first. Precinct 1’s mixed-use neighbourhood centre (east of Springacre) is the early anchor for convenience retail, medical and a first childcare centre (~100–120 places) embedded in the centre heart. Positioning early here de-risks catchment, visibility, access and shared trips.

Growth runway. As additional neighbourhoods and future school sites come online under the Scheme, second and third centres will be viable, likely co-located near primary schools/district centres.

Design & approvals. EDQ uses its Guidelines (Residential 30, Neighbourhood Planning & Design, Centres, Community Facilities). Submissions that read like complete, place-integrated solutions (walkable access, active frontages, safe drop-off loops, acoustic treatments, koala-safe fencing, EV-ready, green roofs/shade) will move faster.

Risks to manage. Koala/ecology overlays near Eprapah, Springacre Rd staging and turn treatments, ILUP→Scheme policy refinements, and DCOP rates yet to be set. (Community groups are closely scrutinising habitat outcomes. They are very active and well-organised in Redlands.

Intelligence to keep live (weekly)

EDQ DAD portal: Track DEV2025/1656 and any new PDA lodgements (precinct plans, traffic, housing strategy updates).

EDQ “Have Your Say”: Capture scheme drafts, infrastructure plan/DCOP details, and any school site indications the moment they surface.

Landholder movements: Urbex/Harridan releases and sales program timing.

Council signals: Redland’s advocacy on busway/rail/arterials asthese influence centre access and catchment.

📣 FOR PRINCIPALS ONLY

Optivest Project Partners is a small, invitation-only group of developers, operators, and investors delivering high-quality childcare centre projects in growth locations nationally.

We leverage location intelligence and pool site opportunities to fast-track deals — working collaboratively to:

Secure prime locations aligned with operator demand

Deliver quality projects with sustainable, long-term value

📞 More? Contact Jeff Gardner | 0402 359 305

📍 WA: East Wanneroo: Perth’s Next Big Leap

Govt promises faster delivery. But will history repeat?

📈 What’s happening WA’s biggest new suburb plan, East Wanneroo, is now officially underway.

The structure plan unlocks 50,000+ new homes, 150,000 residents, and 16 new primary schools across a 2,200-hectare corridor in Perth’s fast-growing north.

👀 The pitch: “We’ve learned from Ellenbrook.”

🛣️ Why it matters WA's planning system has long struggled with fragmented land ownership, slow infrastructure rollouts, and housing affordability.

Ellenbrook was a case study in delays, disconnects, and what not to do.

East Wanneroo aims to fix that:

$1B infrastructure plan: Shared funding model between State, developers, and local government.

Staged rollout: Initial precincts include Sinagra, Tapping, and Pearsall expansion.

New development agency: Delivery Coordination Group to streamline approvals and resolve bottlenecks.

⚠️ But…

No binding infrastructure delivery timelines yet.

Key developers still unclear in some sub-precincts.

High costs per lot risk undermining affordability goals.

🏗️ Developer Watch ✅ Active: Richard Noble, LWP, Stockland, Satterley circling. 📍 Early action in Cell 1: Tapping & Ashby 📍 DA activity starting in Cell 2: Landsdale North & South

🚸 First-Mover Advantage Childcare, health, and community services have clear white space:

No established centres within most PSP precincts.

High birth rates, young families forecasted.

Long buildout = early operators can entrench.

🔁 Sound familiar? In Ellenbrook, early developers held power, but services lagged for years.

If East Wanneroo truly wants to avoid the same fate, fast-tracked service approvals, co-located amenities, and pre-committed operators are essential.

🏗️ Middle Ridge, Toowoomba 112-Place DA

A deep dive into planning intricacies for developers, operators & active investors.

📰 What’s Happening

112 licensed places on a 2,700 m² Ramsay St, Middle Ridge site

Features: 850 m² building (partial 2nd storey), 800 m² outdoor play, 32 bays (19 staff + 12 visitor + 1 PWD)

Large suburban ELCs face intense scrutiny, with parking, noise, neighbourhood character and even “lack of need” objections often stalling or derailing development applications.

⚙️ Traffic Design Essentials

What it does: Ensures safe in/out flow, avoids street queuing.

Parking ratios: 1 bay/3.43 kids basis → 32 bays total

Turn-around bay: 6 × 6 m hammer-head for forward egress

Trip modelling: 0.66 AM & 0.48 PM trips/child → ~74 AM & 54 PM trips over 2 hrs (no stacking lanes needed)

Driveway & sightlines: 6.2 m two-way crossover + 2 × 2.5 m pedestrian triangle

Do this: • Submit swept-path for RCV, SUVs & school buses • Show <15 cars/15 min peak; avoid formal stacking bays • Front-load parking-demand study & management plan

🔊 Acoustic Design Essentials

What it does: Keeps play noise under limits.

Ambient survey: Day 42 dB(A), Eve 43 dB(A), Night 34 dB(A)

Modelling: ISO 9613-2 & SoundPLAN; sources from doors, engines & children (78–87 dB(A))

Barriers: 2–3 m acoustic fences + planting buffers at 4 key receivers

Ops controls: Outdoor play limited 7 am–6 pm; caps per age area (14, 20, 22)

Do this: • Include full noise-modelling report in DA • Specify barrier heights & materials • Attach a Noise Management Plan (monitoring & complaints)

⚖️ Community & “Need” Objections

Push-back themes: Parking overflow, bulk, amenity

Precedents: Glenvale 135-place DA → court appeal; Dundas Valley 44-place DA → “unacceptable”

Planning scheme: No formal “need test” in Toowoomba, but objectors can cite lack of community demand under merit assessment

Do this: • Voluntarily include a Market-Need Statement (0–4 cohort forecasts, occupancy rates) • Share catchment data & vacancy stats in DA docs • Pro-actively consult neighbours via letter-drops or info sessions

📊 Community or Economic Need?

A Needs Assessment cements your case: it quantifies local demand, benchmarks against peer centres, projects forward-supply gaps, and shows council you’ve rigorously proven there’s a genuine community and economic need.

269-273 Ramsay Street (Middle Ridge), Toowoomba Q | Main Service Area ~ 4 min Drive Time, Wed mornings @ 8am | 2km radius shown for context

Comprehensive Needs Assessment: • Detailed 0–4 demographic forecasts • Supply-demand analysis, competitor occupancy & vacancy trends • Pipeline risk weighting (DA-approved vs under-construction) • Market-need justification to head off “oversupply” objections

Engagement-Ready: pre-lodge letters, info sessions

Monitor: “Your Say” & P&E Court for objections

Bottom line: Pair rock-solid traffic & acoustic plans with a real, comprehensive Needs Assessment so neighbours, planners and investors all gain confidence that a centre is both viable and genuinely needed. No point fooling yourself either.

🏡 QLD: Big Push in Canungra: 742ha Proposal Could Reshape the Region

Why it matters

A newly formed consortium of landowners known as Canungra360 has begun consultation on a 742-hectare land release just 4 km north of town.

If approved, it could deliver thousands of new homes in the Gold Coast Hinterland, triggering major planning needs for community, retail, and early years infrastructure.

📊 What Could It Yield?

Based on 2.5 people per dwelling and 6.3% of population aged 0–4.

🧸 Childcare Context: Room to Grow

Canungra, SEQ - 3 km radius outlined in red

The entire 3 km Canungra catchment is served by just one Long Day Care centre: 📍 Milestones Early Learning Canungra – 50 approved places, Meeting NQS across all areas. 💸 Fees: ~$154/day for under-3s, $149/day for 3–5s.

No additional LDCs, either existing or in planning, across the local radius. No current need for more.

📈 What Changes with Canungra360?

If the 742ha plan proceeds:

A population influx of 14,800–27,800 would shift Canungra from small rural town to regional growth hub.

Using standard planning benchmarks (1 LDC per ~10,000 residents), the new community would likely support 2–3 new centres, in addition to the existing 50-place Milestones service.

CREW Insight: There’s no current oversupply, but also no capacity buffer. First-mover developers could pre-position for childcare demand that doesn't yet exist, but almost certainly will.

🧠 CREW Take

This is a greenfield land play of strategic scale:

No pent-up childcare demand today.

But housing-led population growth would rapidly trigger early years infrastructure needs.

CREW readers, especially operators and developers, should monitor: ✅ Rezoning outcomes ✅ Staging timelines ✅ Community node allocations

📍 Milestones is just the start. This could be a 3–4 centre town within 5–10 years.

🆕 New DAs This Week

🏗️ Thornbury VIC 3071 Child Care Centre 📍 323 Darebin Road Thornbury VIC 3071 📅 11 Aug 2025 🔗 Info (Darebin City Council)

🏗️ Augustine Heights QLD 4300 New Child Care Centre 📍 7002 Keidges Road Augustine Heights 4300 QLD 📅 11 Aug 2025 🔗 Info (Ipswich City Council)

🏗️ Auburn NSW 2144 Alterations & Additions to Child Care Centre 📍 50-52 Susan Street, Auburn NSW 2144 📅 11 Aug 2025 🔗 Info (Cumberland Council)

🏗️ Granville NSW 2142 New Child Care Centre 📍 6-8 Factory Street, Granville NSW 2142 📅 8 Aug 2025 🔗 Info (Cumberland Council)

🆕 Service Approvals — 1 Aug to 15 Aug 2025

📅 10 Aug 2025

✅ Tadala Montessori — Joondalup WA — 30 places ✅ Kids Club Paddington — Paddington QLD — 106 places ✅ Amara EL — Balga WA — 104 places ✅ Discovery Tree Springvale — Clayton South VIC — 104 places

📅 5 Aug 2025

✅ Bright Beginnings Turvey Park — Turvey Park NSW — 59 places ✅ Aspire Smiths Lane Clyde North — Clyde North VIC — 126 places ✅ Aspire Huntly Village — Huntly VIC — 88 places ✅ Kiddiwinks Play Laugh & Learn Marsden Park — Marsden Park NSW — 98 places ✅ Pooh's Place ELC Lilydale — Lilydale VIC — 110 places ✅ Aspire Arramont, Wollert — Wollert VIC — 142 places

📅 4 Aug 2025

✅ Condell Park North Montessori Academy — Condell Park NSW — 58 places ✅ Jenny's ELC Grovedale — Grovedale VIC — 120 places

📊 Totals — 1–15 Aug 2025

Total places approved: 1,145

By state:

VIC: 690 places

NSW: 215 places

WA: 134 places

QLD: 106 places

💬 Parting Thought

James Clear nails it:

Running one mile has more in common with running a marathon than sitting at home. Every race starts with one step. Every fortune starts with a small deposit.

Every book begins as one sentence.

The real question is not ‘What is my current position?’ but rather, ‘What is my current trajectory?’

Doing nothing builds nothing.

Put yourself on the path to something better.

Start small, but make sure you start.

CREW take: In childcare real estate, “one step” might be pulling a market report, walking a prospective site, interrogating planning documents, or calling an operator you’ve been meaning to connect with.

The gap between doing nothing and doing something is massive, and momentum compounds.

Don’t wait for the perfect project, partner, or market conditions.

In this sector, the winners aren’t the ones who find the flawless opportunity; they’re the ones who start, refine along the way, and build relentless momentum.

📆 Fri, 3 October 2025 | MLB | Fine 12° Good morning 👋 Morayfield’s Oakey Flat Rd can likely support two ELCs. Sydney just set a childcare price record near $16m at ~4.4%. Supply is rising, demand is steady, and the 2026 three-day guarantee is the wind at our back. In today's edition...🧒🏽 Morayfield: Room for two new ELCs?🏆 Sydney childcare sale sets new Aussie record🍼 New Journey Early Learning: St Albans, VIC📊 Childcare: supply up, demand steady-to-soft 🧸 Childcare deals wrap: September 2025...

📆 Fri, 26 SEPT 2025 | MLB | Showers, Windy 13° Good morning 👋 A regulator steps in at Bright Days Herston as NSW’s pipeline shifts. We’re tracking the outliers, a fresh childcare DA in Yandina, and what Arena’s 2025 signals for community-first investing.In today's edition...🏚 Bright Days, Herston: Enforced Closure✈️ Outliers & Outperformance🏙️ NSW Major Projects🏗️ New DA Lodged: Yandina📊 Insights from a $100B Playbook🏗️ Arena REIT 2025: Annual Results📢 Childcare DA Checklist📈 New DAs and...

📆 Fri, 19 SEPT 2025 | MLB | Showers, Windy 13° 🖐️ Good morningIf you want a plant to grow, you can fuss over it every day; watering, weeding, shifting it toward the sun. Or you can place it in the right soil and let nature do most of the work. A seed planted in the right spot often thrives on its own. Childcare development is no different. You can pour in effort — capital, consultants, marketing — but if the market or site is wrong, it will be a struggle. Put the same energy into picking the...